My name is Laura. I’m a 23-year-old recent college graduate, and “adulting” is still a challenge for me. The biggest challenge of all? Financial responsibility.

I finished school recently, and since then I’ve learned that balancing finances and fun can be seriously difficult.

I live in Miami, Florida but I’m from a small town in the middle of the state. The transition has been exciting, but I’ve also learned that living in a big city comes with a price.

When I was in college, I was financially supported by my parents, which allowed me to keep my head above water and still have fun. Once I graduated, though, that cord was cut.

Now I’m learning how to balance finances on my own. I’ve never considered myself a particularly money-savvy person, but once I had to pay my own bills, I had to learn fast.

I spent a lot of time asking others and the internet for advice on how to make my money go further and avoid spending it all as soon as I earn it.

Watching friends go out and enjoy all the fun nightlife in Miami without joining them is hard. But what’s harder is joining them, checking my bank account the next day and realizing I can’t afford groceries that week.

After doing that once or twice (or three or four times), I finally decided to implement some budgeting apps to control my finances.

Here are my favorite tips on how to manage your money better:

1. Start Tracking Your Spending

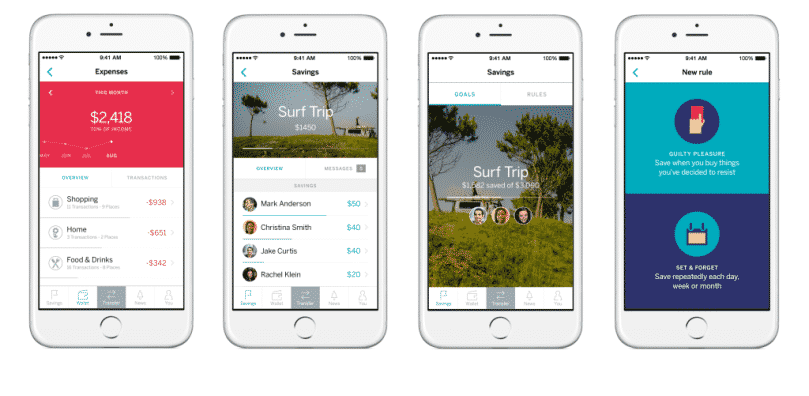

The first thing I did was to download the Mint app. This is a financing and budgeting tool that tracks what I spend and what I have. I linked my bank account, savings account and credit cards to the app.

Now, it tracks all my purchases for me, lets me set a budget and shows me a pie graph that categorizes my spending. It even totals up my cash and debt to show me how much I really have.

I’ll admit that it was really hard to use this app at first. I had to confront the balances I had on my credit cards and the fact that it was almost as much as I had put away in savings. I wasn’t really saving anything. I was just building up debt with interest.

After a couple of months of using the app, I realized that a ton of my money was going to eating out, which was way more than I realized. I was literally blowing my restaurant budget by more than $200 a month.

Once I could see what was happening to my income, I realized I had to start cooking more and ordering out less and started using tips from blogs that helped slow down the flow of spending.

I can now see on the app that that less of my money is going towards eating out. Most importantly, since I’m not adding new restaurant charges to my cards all the time, I’m actually seeing my total debt go down.

Getting a visual representation of how my finances are improving motivates me to keep doing better.

2. Buy a Car, Don’t Lease One

Miami isn’t a walking city. When I was attending college, I almost chose an online college but I lived close enough to school that I could rely on public transportation or my own two feet.

As a working adult, I need a car to get anywhere in the city. I got a lot of conflicting advice on how to get a vehicle. Some people told me that leasing a car would be my best option since I don’t have a lot of experience maintaining one on my own. Plus, a lease allows me to have a lower monthly payment while driving a nicer car.

However, I decided to finance a cheaper car, instead. There were a couple of reasons for that. For one thing, I have a pretty good credit score, which means I can get decent interest rates compared to someone with a low score. As a result, I can still get a good monthly rate for a decent car. I can also save on car insurance with a cheaper car.

Plus, I realized that a car could be an investment. Unlike with leasing, I would own the car after I paid it off and can keep driving it. With a lease, I would pay all that money and at the end, I would have to return the car and sign another contract to keep driving it.

The reality is I will probably consistently need a car for the next few years. If I do move somewhere where I don’t need a car, I would have the option to sell it and actually make some money.

Plus, I’m young, and I’m having fun. Leases come with strict mileage requirements, and I don’t want to either restrict myself to less than 12,000 miles a year or pay a bunch of fees for driving more than that. I plan on taking a few more road trips before I settle down.

By purchasing a car instead of leasing one, I’m not spending money for the restricted experience of temporarily driving a car. I am actually purchasing something of value to own.

Related: How to Shop for a New Car Insurance Policy

3. Stash Money Automatically

Historically, I’ve treated my savings account as a backup checking account. If I felt guilty about how low my checking account got, I would just pull cash out of the savings account I maintained with the same bank.

I wasn’t replacing that money as often or as substantially as I was taking it. That wasn’t working, and my savings failed to grow.

Luckily, I found out that there are lots of different apps available that work as auto-savers. They all have different features and benefits.

I started using the Qapital app to automatically transfer money from my checking account into a savings account I keep with Wells Fargo. I cannot access the funds in person or through an ATM.

If I want to take cash from my Qapital account, I have to transfer it electronically and that can take several days. Since it takes time to get the money, I don’t take it out impulsively.

My parents warned me that a little app like that couldn’t really save enough, but it’s all about how you use it.

Qapital lets you adjust the settings, called “rules” on the app, to modify how much you save. For example, I have to use a rule called “Guilty Pleasure” in which I give myself a $15 weekly budget.

If I don’t go to McDonalds that week, all $15 gets saved automatically. If I visit McDonalds and spend $6, only $9 gets saved. There is also a “Round-up” rule that automatically rounds up the cost of each of my purchases and puts the difference into my savings account.

If I spend $11.25 at a store, that last 75 cents gets socked away. I even have a “Pay Day” rule that automatically stores 5 percent of my paycheck.

All these little rules add up to major savings. Within a few months, I had $2,000 sitting in my savings account and I had taken out exactly $0.

4. Plan for the Future

Right now, I have three goals for my financial future:

- In the short term, I want to enjoy my youth and travel a bit.

- In the medium term, I want to buy a home somewhere I love living.

- In the long term, I want to retire.

I have taken steps to prepare for all these goals. For the first goal, I’ve done a couple things. First, I’ve set up a small savings goal within the Qapital app for travel.

This is where I intend to save up a small fund I can draw from for plane tickets, hostel rooms and other travel expenses. Additionally, I receive airfare alerts that allow me to track when tickets are cheapest. This allows me to plan for trips in the near future.

Qapital is a personal finance mobile application for the iOS and Android operating systems. The app is designed to motivate users to save money through gamification of their spending behavior. Qapital is a full-service banking app that helps its members save smartly and invest confidently, all so they can spend happily.

For the second goal, I plan on building up a down payment for a home. I know that can be substantial and expensive, so on some level this will be a priority. I don’t want to buy a house anytime soon, though, so I have at least five or six years to build up this fund.

Although I can take advantage of affordable housing programs or buy a home without a down payment, having one can make the terms significantly more attractive. I know I want to buy a house, so I’m going to try to save that down payment now rather than hoping I can get good terms without one.

Finally, I want to retire later in life. My workplace offers a small 401(k) match, so I’m saving 6 percent of my paycheck every month. It’s not very much and it could be more, but I know it will build up over time.

Since the money is saved before I get paid, I don’t have to decide to put it away. It’s put away for me, and my savings will continue to grow with every paycheck.

Saving a ton of money means that in practice, my paycheck does not go very far. I have to be frugal with some expenses. But I know that I’m planning for the long term. The money isn’t disappearing.

It’s growing, and eventually I will use it. In the meantime, I’m taking advantage of the free entertainment in Miami as much as possible and spending responsibly when I do go out.

Before you go, you might be leaving free money on the table. Sign up for a few of these apps and you could pocket $250+ this month just for playing games and completing simple tasks. Most people start earning within minutes. See all verified apps here, free to join.

{kind=link}