- See whether a fund is actually worth buying before you put money in, with independent star ratings, fair value estimates, and analyst verdicts

- Run X-Ray on your whole portfolio to catch overlapping holdings, hidden fees, and concentration risk dragging down your returns

- Built for long-term and retirement investors, not day traders, so the research matches how you actually invest

If you landed here, you probably have $50K to $500K invested across a 401(k), IRA, and maybe a taxable brokerage. You hold a handful of funds you can't remember why you bought. You've seen Morningstar's star ratings on Fidelity or Vanguard fund pages. Now you're wondering if it's worth $249 a year to subscribe to the full thing.

Short answer: yes, if you'll actually use it.

I'm subscribed to Morningstar Investor. I've also paid for Zacks, Motley Fool, Seeking Alpha, and Stock Rover at different points so I can tell you exactly where Morningstar fits and where it doesn't. This is the honest review I wish I'd had before I signed up.

The 60-Second Answer

Morningstar Investor is worth $249 if you have at least $50,000 invested, you hold individual funds, ETFs, or stocks (not just one target date fund), and you'll spend 30 minutes a quarter looking at what you own.

Skip it if your whole portfolio is three index funds you'll never touch, your account is under $20K, you want a “buy this Tuesday” pick list, or you actively trade.

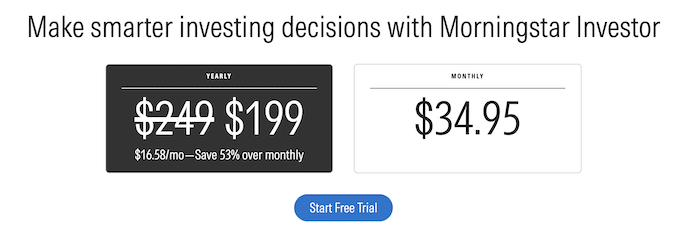

- Price: $249/year or $34.95/month. First year drops to $199 if you sign up through my discount link (auto-applied at checkout).

- Free trial: 7 days. Card required. Auto-renews on day 8 with no warning email.

- What you get: Analyst reports on 1,500+ stocks and 1,600+ mutual funds, Portfolio X-Ray, screeners, and Morningstar's Star, Medalist, and Economic Moat ratings.

- My rating: 4 out of 5 stars. Best-in-class fund research at a retail price. Pays for itself in year one for most subscribers.

→ Try Morningstar Investor (7-Day Free Trial)

Who Actually Benefits from Morningstar Investor

Here's the honest breakdown. Five different people land on the pricing page for five different reasons. Only some should subscribe.

The 401(k) holder who's never audited their funds: Subscribe

You have $80K to $300K in a workplace plan, picked five funds from a menu years ago, and suspect some of them are mediocre. Morningstar Investor was built for you. You'll plug your holdings into X-Ray, read the analyst report on each fund, and have a swap list within an hour. Identify one bad fund to replace and the subscription pays for itself many times over.

The DIY investor firing a 1% advisor: Subscribe

You've been paying somebody $4,000 a year on $400K to manage what's mostly index funds anyway. $249 for Morningstar is rounding error against the $3,750 you're saving. The analyst reports and X-Ray give you the same framework an advisor would use to recommend funds.

The Buffett-style stock picker: Subscribe

You buy individual stocks. You think in moats and intrinsic value. This is the cheapest analyst-grade Fair Value and Moat Rating coverage you'll find anywhere. As of 2025, the Morningstar Wide Moat Focus Index has beaten the broad US market by ~2.5% annualized since 2007. If that framework speaks to you, you'll get your money's worth in a year.

The 3-fund Boglehead: Skip

VTI, BND, VXUS, rebalance once a year, you're done. Morningstar can't make a Boglehead a better investor. Save the $249.

The beginner or active trader: Skip (for now)

If you have under $20K, want someone to tell you what to buy, or trade weekly, this isn't the right tool. Beginners should look at Motley Fool Stock Advisor ($99 first year) instead. Traders should look elsewhere entirely (no charting, no technicals).

What You'll Actually Use It For

Every review online lists Morningstar's features. That's useless. Here are the four things people actually use Morningstar Investor to do.

1. Audit funds you already own

This is the #1 use case. You enter your holdings, run X-Ray, and find out:

- Which of your funds are Gold/Silver/Bronze rated (Morningstar thinks they'll beat their benchmark) vs Neutral/Negative (swap candidates)

- Your weighted average expense ratio across the whole portfolio

- How concentrated you actually are in US large-cap tech (almost always more than you think)

- Whether your “diversified” mix of 6 funds is actually 6 funds holding the same 50 stocks

2. Research a fund before you buy it

Search a ticker, pull the analyst report. You get the Medalist Rating, manager tenure and track record, the firm's quality, fee analysis, and a list of comparable funds in the category. Five minutes versus an hour digging through the prospectus.

3. Pick individual stocks using a Buffett-style screen

Every stock under analyst coverage has a Fair Value Estimate, Moat Rating, Uncertainty Rating, and Capital Allocation Rating. My screen: Wide Moat + 4 or 5 stars (trading below Fair Value) + Low or Medium Uncertainty + Exemplary or Standard Capital Allocation. Spits out 10 to 20 names on any given day worth a closer look.

[Image: Sample analyst report showing Bulls Say / Bears Say sections, Fair Value Estimate, and Moat Rating]

4. Build a portfolio from scratch

If you just got a windfall and have to deploy $100K+, use Morningstar's “Best Investments” curated lists. Best Stock ETFs, Core Medalist ETFs, Best Index Funds, Exemplary Stewards with High Dividends. Pick three or four across categories and you've got a defensible portfolio in under an hour.

How Much Morningstar Investor Costs (and the discount that actually works)

One product, one price, a few discounts if you qualify.

- $249/year billed annually ($199 first year via my discount link)

- $34.95/month billed monthly

- Student: 90% off (~$25/year)

- Teacher: 60% off (~$99/year)

- Military: 30% off (~$175/first year)

Pay annual unless you genuinely only need it for 2-3 months. Three months on the monthly plan is already $105.

The faster way to think about it: identify one mediocre fund to swap (a typical swap saves $300+ a year in fees, forever), and the subscription has paid for itself for the next decade.

How the 7-Day Free Trial Works (and the trap to avoid)

The trial is real and worth using. Here's how it works.

- You sign up at morningstar.com/mm/investor

- You enter a credit card (required, not optional)

- You get full access for 7 days

- On day 8 your card is charged for the annual subscription ($249 standard, or $199 if you signed up via the discount link) unless you cancel

The trap: Morningstar does not send a reminder email before billing. Multiple users on the Better Business Bureau site have complained about being surprised by the day-8 charge. Set your own calendar reminder on day 6.

How to test it properly in 7 days:

- Day 1: Manual-enter your full portfolio. Don't bother with brokerage linking.

- Day 1 or 2: Run Portfolio X-Ray.

- Day 2-4: Read the analyst report on every fund you hold. Note anything rated Neutral or Negative.

- Day 5: Use the screener to find better alternatives to flagged funds.

- Day 6: Decide. If you have at least one actionable swap that saves you more than $249/year in fees, keep it. If not, cancel.

The Three Morningstar Ratings (and how I actually use them)

Morningstar's whole brand is the ratings. Three of them matter. Worth knowing what each is for so you can use them, not just stare at them.

The Fund Star Rating (don't trust it alone)

The famous 1-to-5 stars you see on Fidelity and Vanguard fund pages. It's purely backward-looking. Wall Street Journal published a 2017 study showing only 12% of 5-star funds were still 5-star five years later.

How I use it: as a filter, not a signal. If a fund is 1 or 2 stars over 10 years, I'm out. Beyond that the star rating doesn't drive my decisions.

The Medalist Rating (this is the real one)

Gold, Silver, Bronze, Neutral, Negative. Forward-looking. Will this fund beat its benchmark over a full market cycle, net of fees? Built on three pillars: People (who manages it), Process (how they invest), Parent (firm quality).

How I use it: if I own a fund rated Neutral or Bronze and there's a Gold or Silver alternative in the same category at a lower expense ratio, I look hard at the swap. That one decision is what makes Morningstar pay for itself for most subscribers.

The Moat Rating (the gold standard for stocks)

Wide, Narrow, or None. Whether a company has a durable competitive advantage that lets it earn above-market returns for years.

- Wide moat: 20+ years of advantage. Microsoft, Visa, Coca-Cola, Berkshire.

- Narrow moat: 10+ years. Starbucks, Disney.

- None: no durable edge.

This is the rating I actually care about. The Morningstar Wide Moat Focus Index has returned 11.5% annualized since 2007 versus 8.99% for the broad US market. That's 18 years of real-world outperformance.

How I use it: my whole stock screen is built around it. Wide moat + 4-5 stars + low to medium uncertainty. That filter has done more for my portfolio than the other two ratings combined.

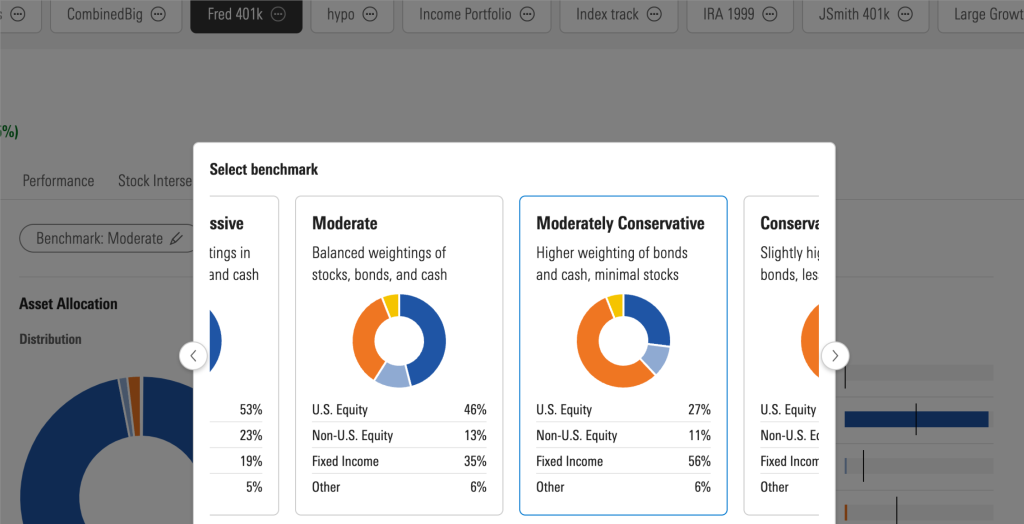

Portfolio X-Ray, the Feature Most People Miss

If you only use one feature in Morningstar Investor, make it X-Ray.

You enter your holdings and X-Ray breaks them down across:

- Asset allocation: stocks vs bonds vs cash vs alternatives

- Stock style: large/mid/small cap by growth/value/blend

- Sector exposure: tech, healthcare, energy, etc.

- World region: US vs developed international vs emerging

- Weighted average expense ratio across all holdings

- Stock Intersection: how much of any single company you actually own across direct holdings + every fund that holds it

Stock Intersection is the killer. It's common to run it and find one mega-cap tech name making up 8-10% of your total portfolio across multiple funds plus direct positions. Most people think they're diversified. They aren't.

UX heads-up: the Stock Intersection table loads in about 4 seconds with no spinner. The first time you run it you might think the page broke. It didn't. Give it a beat.

Morningstar Investor vs the Competition

Morningstar isn't competing with every stock-research subscription. It's competing with whichever one you're considering for the same job. Quick takes.

Motley Fool plays a different game. They tell you what to buy with two new picks every month. Morningstar gives you the framework to decide yourself. Beginners want the first one. Anyone with real money in funds wants the second. I subscribe to both for different reasons.

Seeking Alpha is 16,000 contributors yelling over each other about individual stocks. Lots of breadth on small caps, lots of noise. Morningstar is one in-house voice with deep fund coverage Seeking Alpha doesn't touch. Stock pickers, Seeking Alpha. Fund holders, Morningstar.

Zacks is built for earnings-momentum trading. Different sport. If you swing trade earnings, that's your tool. If you buy and hold for years, Morningstar.

Stock Rover is the dark horse. Cheaper ($180), deeper screener, no analyst opinions. If you think in spreadsheets, Stock Rover. If you want analyst opinions on the funds you actually hold, Morningstar.

What's Not Great About Morningstar Investor

The honest cons. These are the things that make me dock it a star.

- The interface feels like a 2015 enterprise dashboard. Small fonts, dense tables, lots of menus. Functional, not pleasant.

- Performance tracking is broken on linked accounts. Plaid imports the wrong cost basis on most holdings. Manual entry is the answer.

- Ads on a paid product. Minor, but irritating when you're paying $249.

The Bottom Line

After using Morningstar Investor for a while, here's where I land.

One typical fund swap (Bronze actively-managed fund to a Gold-rated index alternative) saves about $342 a year in fees on a $60K position. Forever. That's a 138% return on the Morningstar subscription in year one and pure profit every year after. Most subscribers find at least one swap of similar magnitude in their first month if they actually run X-Ray on what they own.

If you have $50K+ in funds and you haven't audited them in a year, this is one of the highest-ROI tools you can buy. If you're firing a 1% advisor, $249 is rounding error. If you buy individual stocks and like the moat framework, this is the cheapest analyst-grade research you'll find anywhere.

If you're a 3-fund Boglehead, you don't need it. If you have under $20K, the math doesn't work. If you want a “buy this stock Tuesday” pick list, get Motley Fool instead.

The 7-day trial is the real answer. Load your real portfolio, run X-Ray, read the Medalist Ratings on the funds you own. By day 5 you'll know.

How to Sign Up

- Click my discount link to land on the offer page (your $50 off is auto-applied)

- Click “Start Free Trial“

- Create your account

- Enter your card (no charge for 7 days)

- Confirm at the discounted $199 first-year rate

Set a calendar reminder for day 6 if you want to seriously evaluate before being billed.

How to Cancel

- Log in at morningstar.com

- Click your name in the top right, then “Account”

- Go to “Subscription”

- Click “Manage,” then “Cancel”

- Confirm

Access continues until the end of your current billing period. No partial refund for unused days.

- See whether a fund is actually worth buying before you put money in, with independent star ratings, fair value estimates, and analyst verdicts

- Run X-Ray on your whole portfolio to catch overlapping holdings, hidden fees, and concentration risk dragging down your returns

- Built for long-term and retirement investors, not day traders, so the research matches how you actually invest

Frequently Asked Questions

Some plans link, most don't reliably. Skip the linking feature entirely. Manual entry takes 5 minutes and gives you cleaner data than any Plaid import.

Not directly. The “Best Investments” curated lists are essentially Morningstar's top picks per category (best stock ETFs, best dividend funds, best index funds for retirement). You can also get price target notifications that you set up manually.

For investment selection, yes. The analyst reports and X-Ray give you what an advisor would use to recommend funds. For comprehensive planning (tax strategy, estate planning, withdrawal sequencing), you'll still want an hourly advisor for one-off consultations. But $249/year is way cheaper than 1% AUM.

Yes. Ratings are visual and intuitive. Fair Value Estimate is a dollar number you compare to current price. Analyst reports are written in plain English. If you can read a news article, you can use Morningstar Investor.

Two reasons. The star rating is graded on a curve within each category, so only the top 10% are 5-star by definition. And most funds objectively underperform their benchmark net of fees, so most don't deserve high ratings. The whole point is to separate the good from the mediocre.

Same product. Morningstar rebranded Premium to Investor in June 2022 and folded in the free Basic tier. Older reviews calling it “Premium” are talking about the same thing.

You swap them. In an IRA or 401(k), swapping has no tax consequences. In a taxable account, factor in capital gains before selling. Morningstar's “Similar Funds” tool helps you find replacement funds in the same category.

- See whether a fund is actually worth buying before you put money in, with independent star ratings, fair value estimates, and analyst verdicts

- Run X-Ray on your whole portfolio to catch overlapping holdings, hidden fees, and concentration risk dragging down your returns

- Built for long-term and retirement investors, not day traders, so the research matches how you actually invest

{kind=link}